新加坡执行共管公寓

Menu

新加坡执行共管公寓

Buying a home is a long-term commitment, so it is crucial that you do not overstrain yourself financially. Doing thorough research before committing to an Executive Condominium (EC) purchase will help you work out your finances well.

You should:

– Assess your cash and CPF savings to determine your budget

– Plan your cash management for payments, fees, and other costs

– Learn how you can use CPF savings and/or grants

Financing for ECs are typically from banks or financial institutions as HDB does not provide loan for EC purchase. Banks are able to loan you up to 75% of the property value even if you currently have a housing loan (Not applicable for Private property purchase)

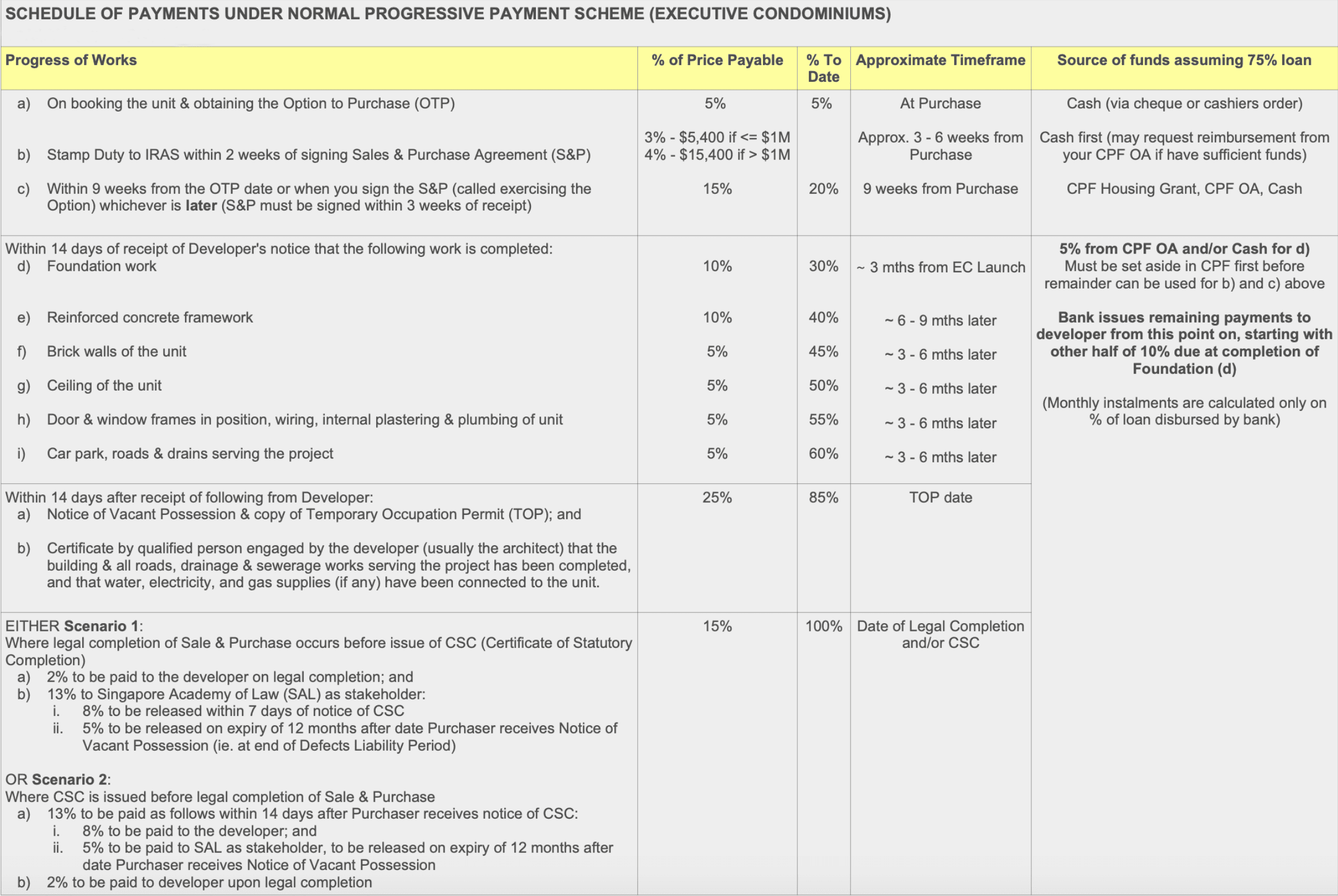

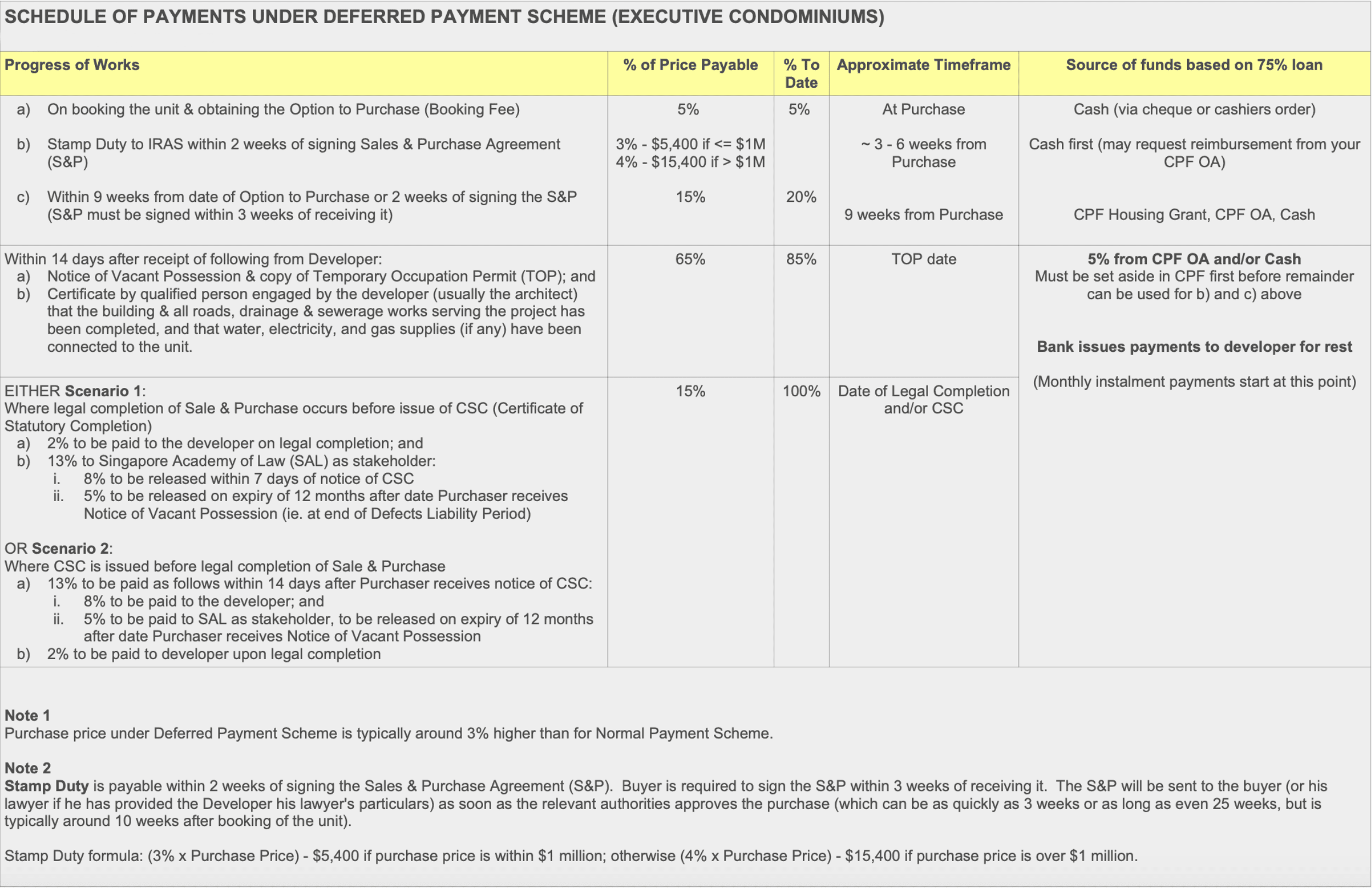

Developer allows buyers to choose either Normal Payment Scheme (NPS) or Deferred Payment Scheme (DPS). Price difference between NPS and DPS is around 3%.

Normal Payment Scheme (NPS), also known as Progressive Payment Scheme, allows you to service your loan via monthly instalments progressively stage by stage as the property is being built.

Deferred Payment Scheme (DPS) allows home owners to start servicing their loan only when the EC is ready for occupation, ie. when owners receive the keys to their EC. DPS is most popular amongst buyers who currently own a HDB and have monthly instalments to service. This allows them to better manage their finances as they do not have to service both loans (HDB & EC) concurrently.

For more information on financing related matters, do feel free to contact us!